RFI Foundation GHG emission Methodology

Introduction:

Our analysis is based on a top-down methodology. We aim to add up all the reported emissions in each country and estimate where they have been financed, whether through bank loans, equity and bonds without double-counting. This creates an approximate mapping of which segments of the financial sector are responsible for financing the most direct emissions and thus identifies those that have the most transition risk if or when these emissions become direct costs for their customers and investees.

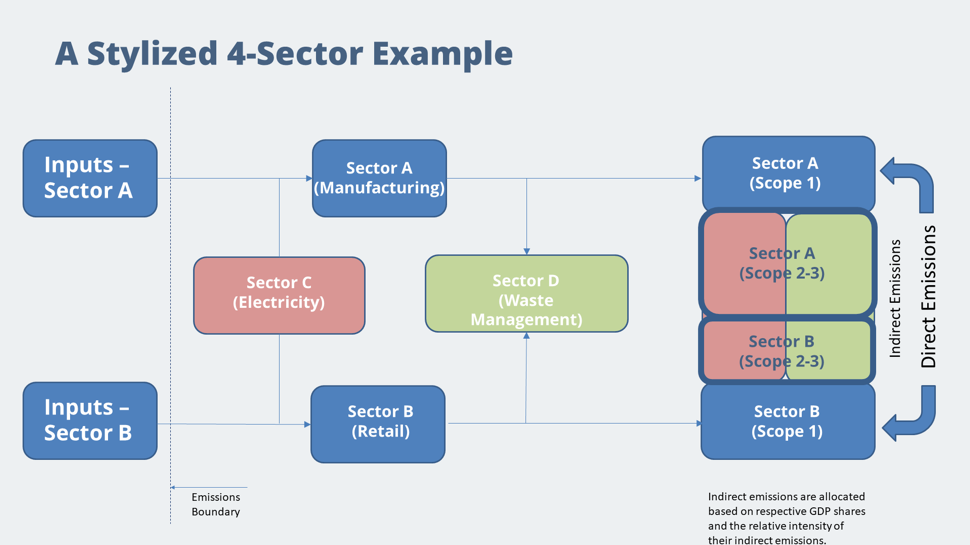

For banks and financial institutions themselves, their Scope 1-2 are limited and are overshadowed by Scope 3 Category 15 emissions. To this end, we consider Scope 1-2 emissions of the financial sector to be zero, while focusing only on Scope 3 Category 15 emissions. Our estimates cover customers’ Scope 1 (direct emissions), Scope 2 (emissions related to electricity used) and Scope 3 (estimated using emissions from transportation and waste management).

We also look deeper to identify indirect emissions to demonstrate how interconnected financed emissions risks are across the financial sector. We identify the sectors whose end-use demand powers the growth of three high emitting sectors (transportation, electricity generation, and waste management) and allocate these indirect emissions to the financial assets that enable them. The indirect sources of emissions that we focus on extend beyond Scope 3, Category 15 emissions under the current GHG Protocol to include other major emissions sources, which is more aligned with the direction that best practice are moving for the financial sector.

We use a top-down methodology based on the “P9XCA” methodology developed by the Finance and Sustainable Development Chair of Paris Dauphine University at the request of Crédit Agricole CIB and published as a Sectorial Guide for the Financial Sector by French environmental and energy agency ADEME (Agence de l’Environnement et de la Maîtrise de l’Energie). The methodology was described by the Institutional Investors Group on Climate Change (IIGCC) and Transition Pathway Initiative (TPI) in their survey of pilot indicators for assessing banks’ transition to Net Zero as a methodology that transparently discloses the assumptions and variables for financed emissions. Its top-down approach works well in data-poor environments which most Islamic markets are today, to complement the company-level data that banks have access to that they are unable to validate as following a consistent methodology for aggregation and reporting.

Methodology:

This top-down methodology takes two data sets, on greenhouse gas emissions and financial assets, in a particular country and matches up categories from each side, with a pro rata split of financial assets (bank loans, bonds and equity) within each economic sector having a proportional allocation of the GHG emissions of that sector.

Bank assets data for financing, loans and advances were collected on a gross basis from the financial statements of banks as of Dec. 31, 2019, or the closest date to that for banks that don’t use calendar year-end data. These data are complemented with aggregated data reported at the same date by each country’s central bank. Bond and sukuk data were compiled from Refinitiv’s EIKON database and news reports through December 2019. The greenhouse gas emissions data are taken from the World Resources Institute’s Climate Watch database, excluding bunker fuels and land use, land use change and forestry (LULUCF).”

Our taxonomy maps capital market assets (equity, bonds and sukuk) organized by top-level sector from each country’s exchanges to our harmonized sector classifications and we align them with the breakdown of GDP economic activity.

GDP data for each country were used as of 2019. We used ‘GDP by Economic Sector at Current Prices’ data for the ‘production view’. Each data set for economic data and financial sector exposures had a separate list of different sectors.

We harmonized the data to match International Standard Industrial Classification (ISIC) to ensure consistency between all our reports. We have made slight adjustments to combine some sectors that account for very small proportions of total financing for improved readability. All this is set up, side-by-side, with the underlying GHG data. Where necessary to break down the GHG data categories into subcategories, we made an allocation pro rata according to the GDP share of each economic activity.

An emissions intensity factor was calculated to account for the fact that industrial sectors use more high-emissions inputs (electricity, transportation and waste management) per unit of GDP than services. Because we use GDP share to reallocate emissions for electricity, transportation and waste management, we need to adjust for the different resource intensities of service and non-service sectors. Therefore, we take the country GDP breakdown between services and non-services and divide the services share by the global electricity share (as a proxy for the other high-emissions inputs) used by services, and divide the residual share of GDP accounted by non-service sectors by the residual electricity share. Next we divide the non-services factor by the services factor to determine the greater proportion of high-emissions inputs used in non-service sectors relative to service sectors which is the emissions intensity factor. It is used to allocate more electricity, transportation and waste management emissions to non-service sectors proportionate to the country-specific electricity emission factor.

Example for Country A emissions intensity factor calculation:

Given that;

- GDP breakdown: 50% services & 50% non-services

- Electricity consumption breakdown: 30% services & 70% non-services

The emission intensity factor for country A is calculated as follows:

- Service Factor: 30% electricity share / 50% GDP share = 0.6

- Non-services factor: 70% electricity share / 50% GDP share = 1.4

- Therefore, emissions intensity factor for Country A would be 1.4 / 0.6 = 2.33

Data Sources:

- GHG data: Climate Watch data: Climate Watch. 2022. GHG Emissions. Washington, DC: World Resources Institute. Available at: https://www.climatewatchdata.org/ghg-emissions.

- Banking data: Each bank’s respective financial statement

- GDP data:

- Malaysia: Ministry of Economy. 2022. National Accounts: GDP by Kind of Economic Activity. Available at: https://www.epu.gov.my/en/socio-economic-statistics/socio-economic/national-accounts

- Indonesia: Bank Indonesia. 2019. Statistics Indonesia: Gross Domestic Product By Industrial Origin. Available at: https://www.bi.go.id/seki/tabel/TABEL7_2.xls

- Saudi Arabia: General Authority of Statistics. 2019. Gross Domestic Product by Kind of Economic Activity. Available at: https://www.stats.gov.sa/sites/default/files/Gross%20Domestic%20Product%20by%20Kind%20of%20Economic%20Activity%20at%20Current%20Prices%202021EN.xlsx

- UAE: Bayanat. 2020. GDP by Economic Sector. Available at: http://data.bayanat.ae/en_GB/dataset?groups=national-accounts

- Turkey: OECD. 2022. Türkiye: Annual Gross Domestic Product. Available at: https://stats.oecd.org/Index.aspx

- Bangladesh: Bangladesh Bureau of Statistics. 2020. Gross Domestic Product of Bangladesh at Current Prices. Available at: http://bbs.portal.gov.bd/sites/default/files/files/bbs.portal.gov.bd/page/057b0f3b_a9e8_4fde_b3a6_6daec3853586/2021-08-12-10-27-179b5340c788c15a44a7032a41ce1776.pdf

- Capital Market (Equity, Bond and Sukuk data): Thomson Reuters Eikon. 2019. Equity, Bonds and Sukuk data. Available at: https://eikon.thomsonreuters.com/index.html

- Emission Factors data:

- GDP data by industry: The World Bank. 2017. World Development Indicators: Structure of value added. Available at: http://wdi.worldbank.org/table/4.2

- Global Electricity data: IEA. 2019. Electricity consumption – Electricity Information: Overview. Available at: https://www.iea.org/reports/electricity-information-overview/electricity-consumption